Tax News & View Excessively Fine Rarebit Roundup

Tax News & View Excessively Fine Rarebit Roundup

11th Circuit says foreign account fines can violate 8th Amendment. Countdown to 2025. Unrealized gain tax - wise, or terrible? Welsh Rarebit Day.

Key Takeaways

11th Circuit says FBAR fines can trigger "excessive clause" constitutional limits.

Split with First Circuit may tee up Supreme Court review.

TIGTA report highlights difficulty of not auditing earners under $400,000.

Where taxes will increase if 2017 tax cuts are allowed to expire.

"Taxing unrealized capital gains is a terrible idea"

"Misleading" Tariff talk.

99 exemptions, 366 days in prison.

Welsh Rarebit Day.

FBAR Ruling Creates Circuit Split Over Excessive Fines Clause - Tristan Navera, Bloomberg ($):

The Excessive Fines clause of the US Constitution’s Eighth Amendment does apply to penalties levied for failure to report foreign bank accounts, the Eleventh Circuit said Friday, creating a split with the only other federal appeals court to rule on the question.

...

The Excessive Fines clause of the US Constitution’s Eighth Amendment does apply to penalties levied for failure to report foreign bank accounts, the Eleventh Circuit said Friday, creating a split with the only other federal appeals court to rule on the question.

Schwarzbaum FBAR Penalty Dispute Results in Circuit Split - Amanda Athanasiou, Tax Notes ($):

The court found $300,000 in penalties levied in Schwarzbaum’s case to be “grossly disproportionate to the offense” of concealing a Swiss account with a relatively low balance, but it approved the remainder of his penalties under the excessive fines clause. The court struck the unconstitutional penalties and remanded the case to the U.S. District Court for the Southern District of Florida, ordering a judgment against Schwarzbaum of almost $12.3 million, plus fees and interest.

...

The court took particular issue with a $100,000 penalty assessed for each year from 2007 to 2009 for an account with a maximum balance of under $16,000 in each of those years. The penalties were grossly disproportionate to the attempt to conceal “at most, roughly $16,000” from the IRS, the court found. It characterized the penalties for all three years as “constitutionally excessive.”

The split between the 1st and 11th circuits makes it much more likely that the Supreme Court will hear the issue.

Link: 11th Circuit opinion No. 22-14058

Fight for $400,000

IRS Work Holding Audits Flat on Under-$400,000 Proves Difficult - Chris Cioffi, Bloomberg ($):

The IRS is lagging on a plan to prevent the agency from boosting audit rates of households and small businesses earning less than $400,000, a Treasury watchdog report finds, fanning skepticism about its ability to do so.

When the IRS received billions in the Democrats’ tax-and-climate law known as the Inflation Reduction Act to boost enforcement, Treasury Secretary Janet Yellen ordered the agency to ensure the money would only be used to police wealthy scofflaws. A Treasury Inspector General for Tax Administration report illustrates the challenges hampering IRS efforts.

It was an unwise but politically-expedient pledge. It gives the (erroneous - see second-to-last item) message that as long as you make under $400,000, you can cheat on taxes because you won't get audited.

Countdown to 2025

Where Taxes Would Rise the Most if Trump’s Tax Cuts Expire - Richard Rubin, Wall Street Journal:

When Congress cut taxes in 2017, it attached a ticking countdown clock that is approaching zero.

If Congress doesn’t act by the end of 2025, income taxes will go up for most households. An analysis by the Tax Foundation shows that, on average, taxes would rise in every single county in the country—urban or rural, wealthy or poor—but the amounts vary, as you will see below. The analysis doesn’t speak to the median household’s tax bill, but it shows how much more people in each area would be paying.

Big Business Ponders Global Tax Strategy as 2025 Cliff Nears - Chris Cioffi, Bloomberg ($):

The 2017 GOP tax overhaul slashed the corporate rate from 35% to 21%. To pay for such a big cut and to spur businesses to bring foreign capital home while continuing to invest in the US, the law enacted international provisions such as GILTI along with other tax base-broadening policies. The hope was to reward companies for moving profits back to the US while slapping them on the wrist if they sent them to lower-tax jurisdictions.

While the law made the corporate rate permanent, it built in a sunset of individual tax cuts and an increase in international tax rates at the end of 2025.

Can Democrats Stop the ‘Tax Doom Loop’? - Andrew Duehren, New York Times:

To try to harden Democrats’ hearts ahead of the talks, the party’s tax experts and academics have been pushing the idea that letting the 2017 tax cuts expire entirely would not be such a bad outcome. They have pointed to soaring deficits and argued that the economy could absorb higher taxes without slowing growth. The goal is to make the party comfortable with the possibility of walking away from talks with Republicans if Democrats don’t score enough victories — and avoid repeating the saga over the Bush tax cuts.

“You do have the card of letting it all expire because, frankly, it’s not going to be that noticeable of a tax increase for middle America,” Kimberly Clausing, a former Treasury official in the Biden administration, said.

Tax on the Campaign Trail

Strategic Ambiguity in the Harris-Walz Tax Proposals - Mindy Herzfeld, Tax Notes ($):

Both the Democratic Party platform and the Final Master Platform are short on policy and heavy on politically popular talking points, with the campaign advisers perhaps recognizing that they have little to gain by elaborating on progressive policy ideas. But examining the outline of the proposals and promises is still useful to consider what economic and fiscal policy in an administration under now-Vice President Kamala Harris and Minnesota Democratic Gov. Tim Walz — particularly as it affects cross-border taxation — might look like. More broadly, the platform hints at how a U.S. international tax policy that adapts after a generational shift and a recognition of America’s changing place in the world could and should take form.

...

The Democratic platform promises to increase the corporate tax rate without specifying by how much, but the Harris campaign has said it will be raised to 28 percent. (Prior coverage: Tax Notes Federal, Aug. 26, 2024, p. 1765.) The latest Biden administration budget also proposed increasing the corporate rate to 28 percent.

Whether such a proposal would come to fruition, even if Harris is elected and even if Democrats controlled both houses of Congress, is an open question. The Biden administration’s efforts to increase the corporate rate in 2021, when Democrats controlled the House and Senate, failed. Sens. Kyrsten Sinema, I-Ariz., and Joe Manchin III, I-W.Va., blocked any corporate rate increase.

Taxing unrealized capital gains is a terrible idea - Tyler Cowen, Marginal Revolution:

Sadly, Jason Furman has been endorsing one of the very worst economic ideas of our generation. Here is Jason’s Twitter take, here is his earlier WSJ piece.

...

Read through Jason’s own words in the WSJ — do you really think a system that complicated is going to reduce tax planning? How about figuring out what percentage of liquid vs. illiquid assets to hold? Whether to finance ventures through private equity vs. public markets? Which risky assets to buy and sell before December 31? How much to put into your foundation, so as to adjust your net wealth status? Might there not be other “tricks” to adjust your tax eligibility as well? What about those “live in Puerto Rico” decisions?

Should we tax realized gains? - Scott Sumner, The Pursuit of Happiness. "In my view, the original sin of tax policy was the decision to focus on income, not consumption. Once we started down that road, we created a system where closing one loophole would inevitably create a couple more. Yes, if income really is the thing that should be taxed, then it makes logical sense to tax unrealized gains. But income is not the right base for our tax system; consumption is what matters."

Trump and Vance’s false and misleading rhetoric on tariffs - Glenn Kessler, Washington Post ($):

First, let’s get this straight: Trump is flat wrong to claim that the entire tariff is paid by a foreign country. And Vance is wrong to suggest there’s a debate among pointy-headed experts about whether tariffs increase prices.

...

Economists agree that tariffs — essentially a tax on domestic consumption — are paid by importers, such as U.S. companies, which in turn pass on most or all of the costs to consumers or producers who may use imported materials in their products. As a matter of demand and supply elasticities, overseas producers will pay part of the tax if there are fewer goods sold to the United States. Domestic producers in effect get a subsidy because they can raise their prices to the level imposed on importers.

A Newborn Tax Credit Could Be Worthwhile, With Sound Administration - Margot Crandall-Hollick, TaxVox. "Parents would receive up to $6,000 for their newborn—a $2,400 boost on the $3,600 ARP child credit for young children under 6 years old."

Don't Bother Me With Details

Congress Put the Wrong Date in the Tax Law. Companies Are Reaping Millions. - Richard Rubin, Wall Street Journal:

The dispute involves Section 245A, the 2017 addition to the tax code that lets U.S. companies bring home their foreign profits without paying U.S. taxes. To make that work, Congress also changed Section 78—designed to prevent inappropriate tax breaks in the old international tax system—in a way that stopped companies from getting a double benefit.

But lawmakers set different effective dates. The new tax break under Section 245A started on Jan. 1, 2018, while the new limits in Section 78 started for companies’ first taxable years beginning after Dec. 31, 2017.

Related: Eide Bailly International Tax Services

Blogs and Bits

Direct File states reach 20, with Maine & Wisconsin joining the IRS free tax prep program - Kay Bell, Don't Mess With Taxes. "When the 2025 filing season starts, more than 120,000 Maine and 600,000 Wisconsin taxpayers and will be eligible to file via the IRS created and managed free, online tax preparation and e-filing option."

Tax Court Narrowly Sides with IRS in Rejecting CDP Hearing for Canadian Taxpayer - Parker Tax Pro Library. "In an issue of first impression, a closely divided Tax Court held that, because a United States treaty with Canada requires the United States to collect an accepted Canadian revenue claim as it would a United States tax assessment for which the taxpayer's right to a Collection Due Process (CDP) hearing (among other rights) has lapsed or been exhausted, a Canadian taxpayer living in the United States has no additional rights under Code Sec. 6320 or Code Sec. 6330 with respect to the IRS's collection of her Canadian tax liability."

Businesses Aren’t Confident About Corporate Transparency Act Compliance - Kelly Phillips Erb, Forbes ($). "Most corporations are aware of the CTA—nearly all (93%) respondents said they were aware that the law existed, but expressed uncertainty about the details. Specifically, less than half (45%) of respondents surveyed are aware of the CTA's reporting requirements."

Related: Corporate Transparency Act Mandates Stricter Federal Disclosures

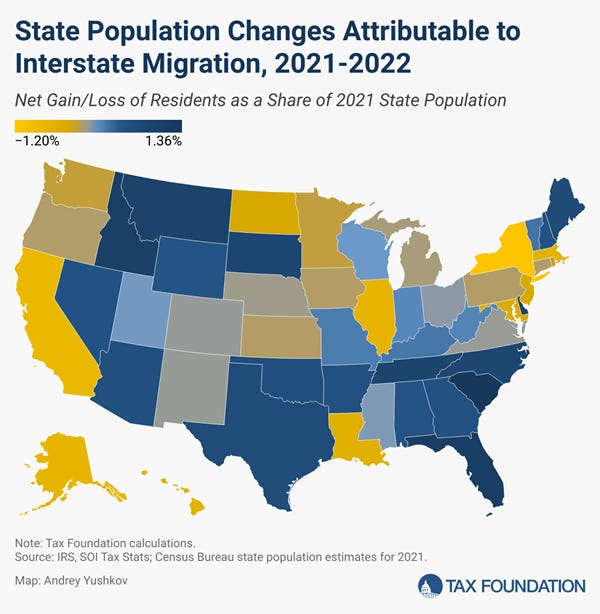

Taxes and Interstate Migration: 2024 Update - Andrey Yushkov, Tax Foundation. "The IRS data show that between 2021 and 2022, 26 states experienced a net gain in income tax filers from interstate migration, led by Florida (+125,551), Texas (+88,216), North Carolina (+43,653), South Carolina (+32,927), and Tennessee (+30,935). Conversely, 24 states and the District of Columbia experienced a net loss, led by California (-144,203), New York (-108,586), Illinois (-45,460), Massachusetts (-26,033), and New Jersey (-20,820)."

Pueblo man sentenced for evading income tax - IRS (Defendant name omitted, emphasis added):

The U.S. Attorney’s Office for the District of Colorado announces that Defendant, of Pueblo, Colorado, was sentenced to one year and one day in federal prison followed by three years of supervised release for tax evasion.

According to the plea agreement, Defendant worked for various employers as a journeyman electrical lineman. Beginning in 2016, and continuing until January of 2020, the defendant willfully avoided paying a substantial amount of income tax by submitting to his employers inaccurate Form W-4s claiming up to 99 allowances or false claims of tax exemptions. During this time, the defendant was only allowed to claim two allowances.

Defendant’s filings caused his employers to withhold little, if any, withholding taxes from his earned income. Although the defendant had an opportunity to pay all taxes due and owing for each calendar year by the respective filing deadlines, he did not file a tax return for any of the years in question. This resulted in the evasion of $267,028.50 in federal taxes. Consistent with his plea agreement, the Court ordered Defendant to pay restitution – inclusive of interest and penalties as calculated by the IRS. That amount is in excess of $548,000.

It's unlikely that this unfortunate journeyman electrical lineman ever made over $400,000, but they still audited him. Not filing when you have W-2 income is something IRS computers notice.

What day is it?

It is National Welsh Rarebit Day. Probably not enough of a holiday to extend the Labor Day long weekend.

About the Author

Joe B. Kristan CPA

Partner

After 38 years centered on tax consulting for closely held businesses and their owners, Joe is joining Eide Bailly's National Tax Office. Joe's responsibilities include communication, process improvement and training. He is a principal contributor to the Eide Bailly Tax News and Views blog, providing daily updates on tax reform and other tax news. Joe is a Certified Public Accountant and a member of the AICPA Tax Section and Iowa Society of Public Accountants.

Follow Joe on LinkedIn.